Q2 2025 saw net inflows of $614.0 billion into managed vehicles, according to data from ISS MarketPulse powered by Simfund Total Market. This served as a slight increase from the comparatively restrained first quarter when funds gathered $486.9 billion. ETFs were the strongest contributor to net deposits in the second quarter, while both mutual funds and CITs saw net inflows surpass $100 billion.

Industry Overview

ETF net inflows in the second quarter totaled $385.3 billion, a more than $200 billion lead over the next highest inflow vehicle. This did, however, represent a slight decline from the $444.1 billion gathered in Q1 2025. Passive ETFs gathered the bulk of net flows at $285.5 billion. Even as active ETFs managed assets of $1.4 trillion, less than a tenth of passive ETFs’ $15.2 trillion, they were remarkably close behind in net deposits for the quarter at $99.8 billion. ETFs based in the United States accounted for the largest portion of inflows within ETFs in the second quarter. U.S.-domiciled ETFs accounted for $144.5 billion in passive Q2 inflows, a nearly $100 billion lead over China-domiciled ETFs ($47.3 billion). U.S. funds were even more dominant among active ETFs, gathering net deposits of $83.6 billion and followed by only $4.4 billion into Ireland-domiciled funds.

Mutual funds experienced the second highest level of quarterly flows at $182.9 billion, a significant improvement from the $10.1 billion in net redemptions seen during Q1. The vehicle has been particularly dependent on money market funds for positive flows in recent quarters. Absent that asset class, long-term mutual funds saw inflows of just $219.9 million in Q2, having faced harsh outflows of $82.7 billion in Q1. U.S.-based money market funds experienced sharp withdrawals in the immediate wake of early April’s widespread tariff announcements, as covered in prior ISS MI research, and ultimately recorded net outflows for the quarter as a whole. Investors in other domiciles looking for safe havens boosted Q2 inflows.

Collective investment trusts increased net commitments to $104.2 billion in Q2 2025 after $77.9 billion in Q1. Allocation funds, primarily in the form of target-date funds, experienced the highest net flows at $58.1 billion, their strongest quarterly activity in two years. Equity funds contributed the second most for the quarter at $31.5 billion.

Retail separately managed accounts recorded positive flows of $12.9 billion in Q2, though this was notably lower than the $50.2 billion seen in Q1 and the lowest period over the past two and a half years. Fixed income funds led for the quarter at $6.3 billion, a sizable drop from inflows of $29.3 billion in Q1. Institutional separate accounts conversely experienced the strongest net withdrawals for the quarter at $71.3 billion, in line with the prior quarter’s outflows of $75.2 billion. Fixed income strategies led inflows for the quarter at $27.3 billion, while equity funds experienced the harshest net redemptions of $92.6 billion.

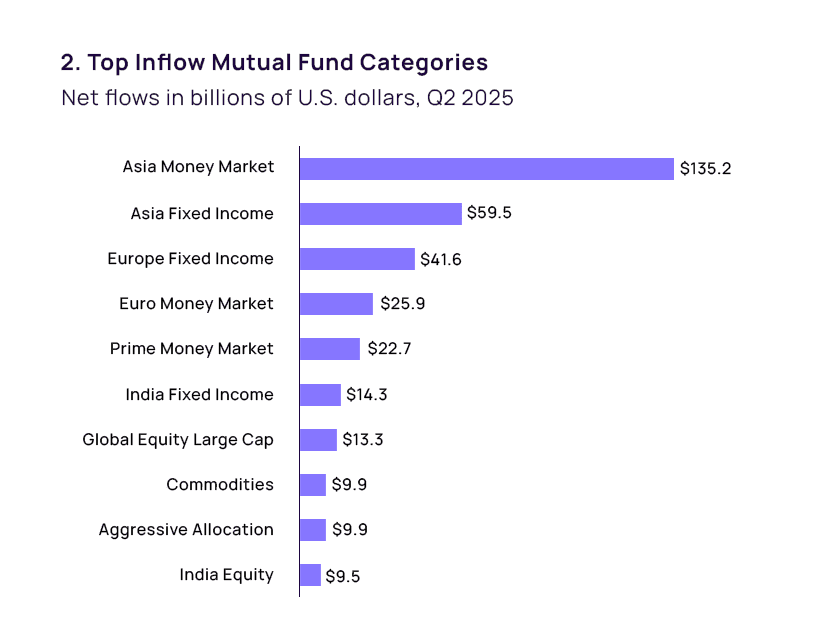

Money market funds were the largest source of mutual inflows over the second quarter. The regions where this occurred, however, saw a drastic shift from prior quarters. U.S.-domiciled money market funds led inflows in the asset class in Q1 2025 at $53.7 billion. This turned to net redemptions of $14.9 billion in the second quarter. China-based money market funds were the lead beneficiary in Q2, experiencing inflows of $110.7 billion after outflows of $41.2 billion in Q1. This was entirely within the Asia Money Market category, which collected net inflows of $135.2 billion, a significant rebound from outflows of $43.4 billion in Q1. The quarter also saw additional net deposits from European money market funds ($25.9 billion) and U.S.-based prime funds ($22.7 billion).

Fixed income strategies accounted for the second highest net deposits in mutual funds at $154.4 billion, an increase from the $92.1 billion the asset class gathered in Q1. As within money market funds, activity was strongest within Asian markets. Asia Fixed Income experienced the second highest inflows for the quarter at $59.5 billion, with funds in the category domiciled overwhelmingly in China. The category had recorded outflows of $70.3 billion the prior quarter. India Fixed Income additionally gathered inflows of $13.3 billion following Q1 outflows of $3.0 billion.

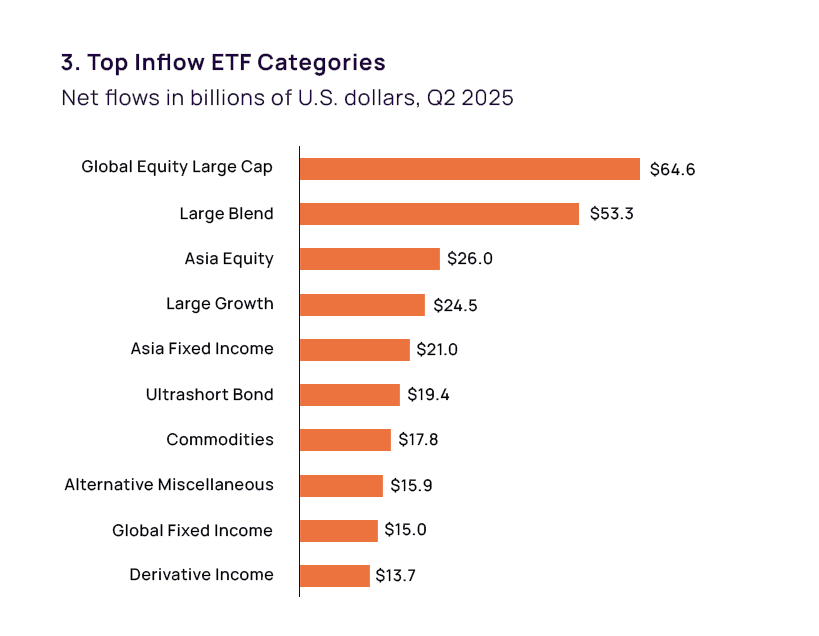

Equity funds were the largest source of flows into ETFs during the second quarter at $202.3 billion, a decrease from the $271.4 billion gathered in Q1. Large capitalization strategies continued to lead demand within the asset class. Global Equity Large Cap pulled ahead of Large Blend, bringing in net deposits of $64.6 billion after inflows of $47.8 billion in Q1. Within Global Equity Large Cap, U.S.-domiciled funds contributed the highest portion of inflows at $36.1 billion, followed by funds based in Ireland and Canada at $18.6 billion and $5.5 billion, respectively. Large Blend funds focusing on U.S. markets experienced the second highest flows at $53.3 billion, down from $95.3 billion in the first quarter. U.S.-based funds led quarterly inflows at $44.0 billion, followed by Canadian funds at $4.8 billion. BlackRock acted as the leading inflow global large cap manager for the quarter at $19.1 billion, followed closely by Vanguard ($17.0 billion). Vanguard recorded a higher relative lead within U.S. large blend funds with net deposits of $37.6 billion, followed by State Street Investment Management ($7.0 billion).

Fixed income also contributed significantly to ETF inflows. Bond ETF net deposits totaled $121.9 billion in Q2 2025, a marginal improvement from $118.6 billion gathered in Q1, if less than the amount gathered by bond mutual funds in the second quarter. Asia-focused funds similarly accounted for the highest flows among fixed income ETFs. Asia Fixed Income saw net deposits increase dramatically from $773.27 million in Q1 to $21.0 billion in Q2. HFT Investment Management acted as the top inflow manager in the category at $5.6 billion, followed by China AMC ($2.6 billion).

Visit the page later this week to see additional insights into Q2 global fund flows, covering retail SMAs, CITs, and separate accounts.

We’re committed to bringing our clients ongoing insights from this expanded dataset and illustrating how this data enables firms to spot opportunities, analyze fund flows across vehicle types, or conduct customized benchmarking. Contact us here or through a Sales or Client Success representative, and visit our MarketPulse site to learn more.

By Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence