At this year’s 529 Conference, ISS MI’s Viraaj Kumar joined Paul Curley, our head of 529, for a panel discussion focused on “Partnership Opportunities to Generate Long-Term Growth.” The conversation featured insights from Matt Golden, SVP and Savings Lead at Vestwell, and Brandon Goeke, Director of Operations at Florida Prepaid College Board, highlighting the evolving savings landscape and emerging opportunities in both education and retirement planning.

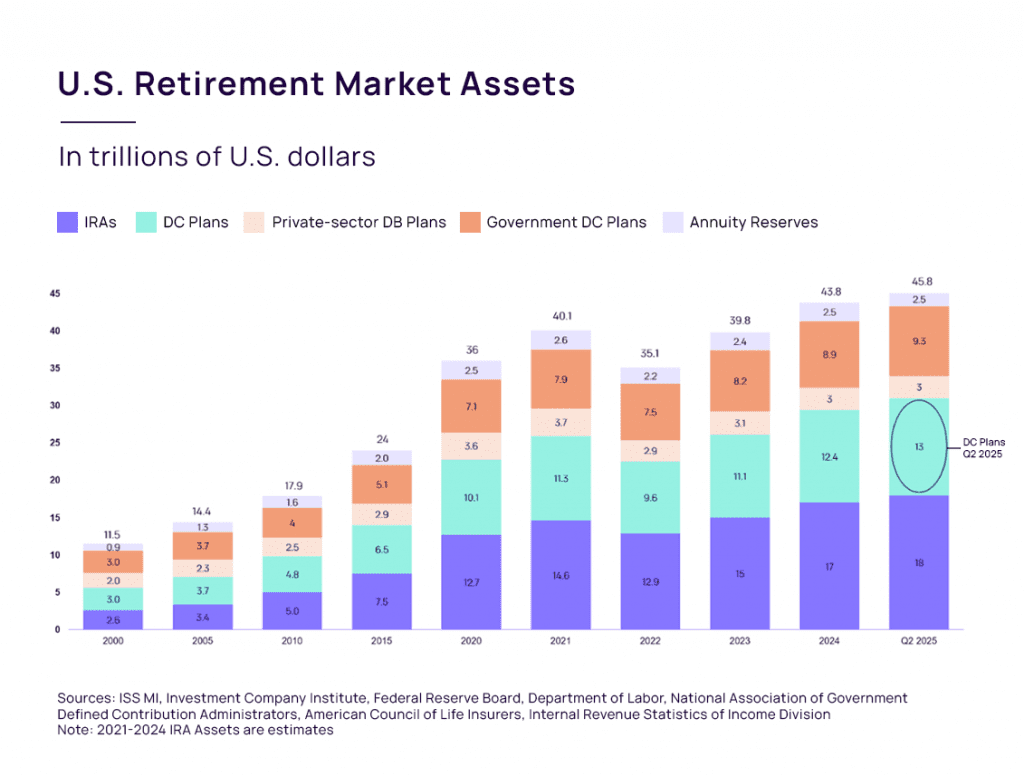

The numbers speak volumes: as seen in the figure below, U.S. retirement assets have reached $45.8 trillion, with DC plans (circled) accounting for $13 trillion in 2025. Yet only 14.5% of U.S. households currently use 529 plans, and more than half of education-related assets are sitting in retirement accounts like 401(k)s and Roth IRAs. This signals a clear opportunity to better align savings strategies with financial goals.

The Case for Integration

There are clear parallels between 401(k) and 529 plans. Both are born from legislation and designed to support long-term financial wellness, but while 401(k) plans have experienced growth through workplace-based plans, 529 plans still have much room for growth. According to the experts on the panel, integrating 529 plans into workplace benefits could unlock broader participation and help families save more effectively for education.

Here are three additional key takeaways from the conference:

1. Retirement Access Gaps Persist Despite Asset Growth

While U.S. retirement assets have surpassed $40 trillion, the conversation emphasized that this growth doesn’t equate to universal coverage. According to the U.S. Federal Reserve, roughly one-third of Americans have no retirement savings, and about a quarter lack access to a workplace retirement plan. For lower-income households, there’s still an overreliance on Social Security, underscoring the need for expanded access and education.

2. 529 Plans Are Poised for Accelerated Growth

Drawing parallels to the early evolution of 401(k)s, the members of the panel noted that the 529 industry is still in its first 25-year phase. With only 14.5% of U.S. households currently using 529 plans, according to a survey from Edward Jones, there’s significant runway for growth. The strong correlation between education and wealth generation positions 529s as a critical tool for long-term financial health.

3. Retirement and Education Assets Are Blurring

A surprising insight from the session: more education-related assets are currently held in retirement accounts (like Roth IRAs and 401(k)s) than in 529 plans. This suggests that many savers may be using the wrong vehicles for education planning, highlighting an opportunity for better guidance, labeling, and product alignment across the industry.

What’s next?

Looking ahead, the panel projected significant growth in the 529 market over the next decade, driven by:

- Better education around savings allocation

- Workplace integrations of 529 plans

- Simplified product offerings

- Collaborative innovation across financial services

ISS Market Intelligence provides market data, insights, events, media, fee analysis, distribution analysis, and a newsletter for the 529 and ABLE industry. To learn how your organization can help support or partner with the 529 Conference, please contact Paul Curley.