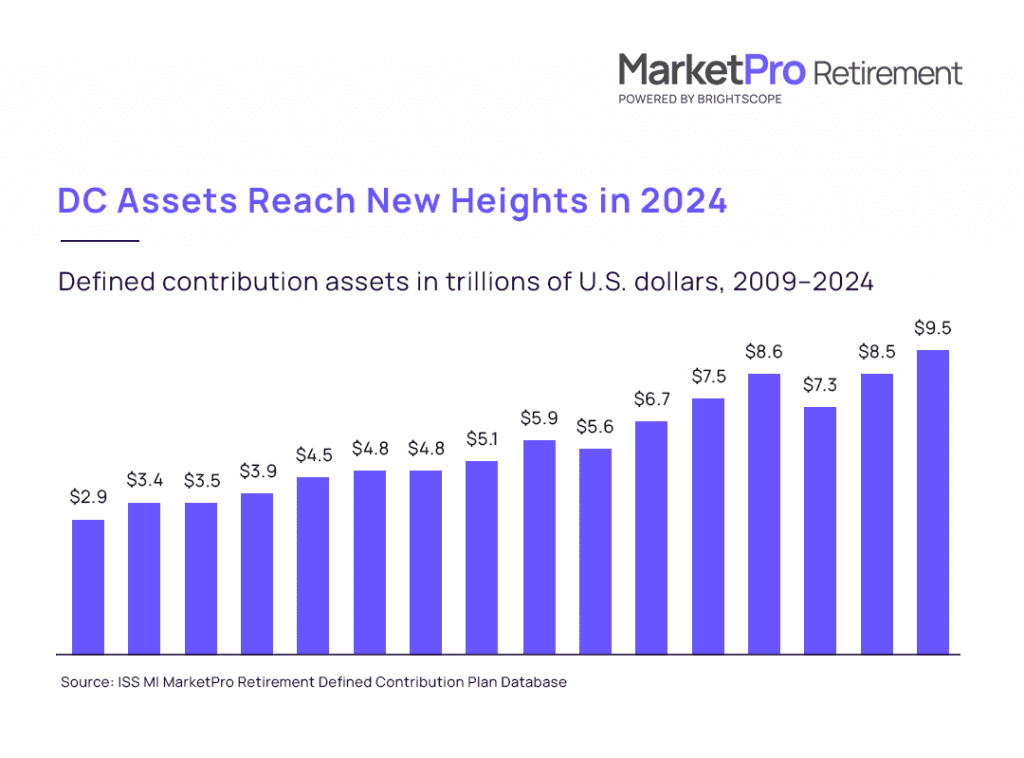

Defined contribution (DC) plans in the aggregate recorded a solid recovery through 2024. Assets in ERISA-regulated DC plans totaled $9.5 trillion at the end of the year, according to Form 5500 data released by the U.S. Department of Labor (DOL) and captured in the ISS MI MarketPro Retirement Defined Contribution Plan database. This represented the second year of more than $1 trillion in asset growth. Total plan assets have nearly doubled over the past decade.

DC plans in 2024 achieved this soaring asset growth primarily through market appreciation. Domestic equity markets saw two consecutive years of 20%-plus performance, with the S&P 500 returning 25.0% in 2024 after 26.2% in 2023. Bond markets struggled across the finish line with returns of 1.2% in 2024, following 2023’s 5.5%, but this was a comparative relief after the -13.0% seen in 2022.

Participation in DC plans also continued to increase at a steady pace. The number of DC plans crossed 800,000, while the number of active participants grew to just shy of 95 million at years’ end. Growth in newer, smaller plans remains critical for addressing the demographic hurdles affecting the broader DC space. As covered in a recent issue of Windows into Defined Contribution, plans with less than $100 million have recorded the largest net inflows in recent years, while the largest, most established plans saw the starkest outflows.

DC stakeholders have expressed strong interest in the multi-employer plan (MEP) and pooled-employer plan (PEP) markets as a means of harnessing and expanding on that potential in smaller plans. ISS MI MarketPro Retirement data found that MEP assets grew to $488.6 billion at the end of 2024. While a small total in comparison to the almost $10 trillion market overall, this represented a 20% increase from the prior year. The number of underlying employers saw an even larger proportional gain, growing from approximately 76,000 in 2023 to 115,000 in 2024.

Even as asset and participant growth moved at a steady pace, retirement plans faced starker outflows. DC net redemptions had moderated across 2022 and 2023 but sank to more than $100 billion in 2024. A more return-to-normal market environment may have eased the pain of withdrawals right as the U.S. hit new demographic hurdles. The year represented the beginning of what commentators have referred to as “Peak 65,” with more than four million Americans expected to turn 65 on an annual basis.

The full report is available to subscribers on the MarketSage research portal. For more information about this report, or any of ISS MI’s research offerings, please contact us.

Author: Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence