Recently approved new structure offers asset managers a new route into the fast-growing ETF market—either to capture new sales or to retain existing mutual fund shareholders that might otherwise defect, says ISS MI’s Christopher Davis.

Since Vanguard’s ETF share class patent expired in 2023, nearly 80 fund managers have petitioned the Securities and Exchange Commission (SEC) for exemptive relief to add ETF share classes to existing actively managed mutual funds.

Earlier this week, the SEC gave Dimensional Fund Advisors—a top 10 fund manager in the U.S. and the country’s largest active ETF provider—the green light to launch ETF share classes. The decision, pending a 15-day comment period, paves the way for dozens of managers to follow, expanding choice for active investors.

The SEC has signaled it will move quickly on approvals. Dimensional’s case now serves as a blueprint, spelling out oversight responsibilities for the firm and its board. In the lead up to the move by the SEC, regulators had flagged concerns like ‘cross-subsidization’—where ETF investors could end up footing costs that belong to mutual fund shareholders. Managers looking for approval will likely need to adopt the latest changes made to Dimensional’s filings, including instituting an ongoing monitoring process to observe costs, staffed with designated board members.

A Win for Asset Managers, but Hurdles Remain

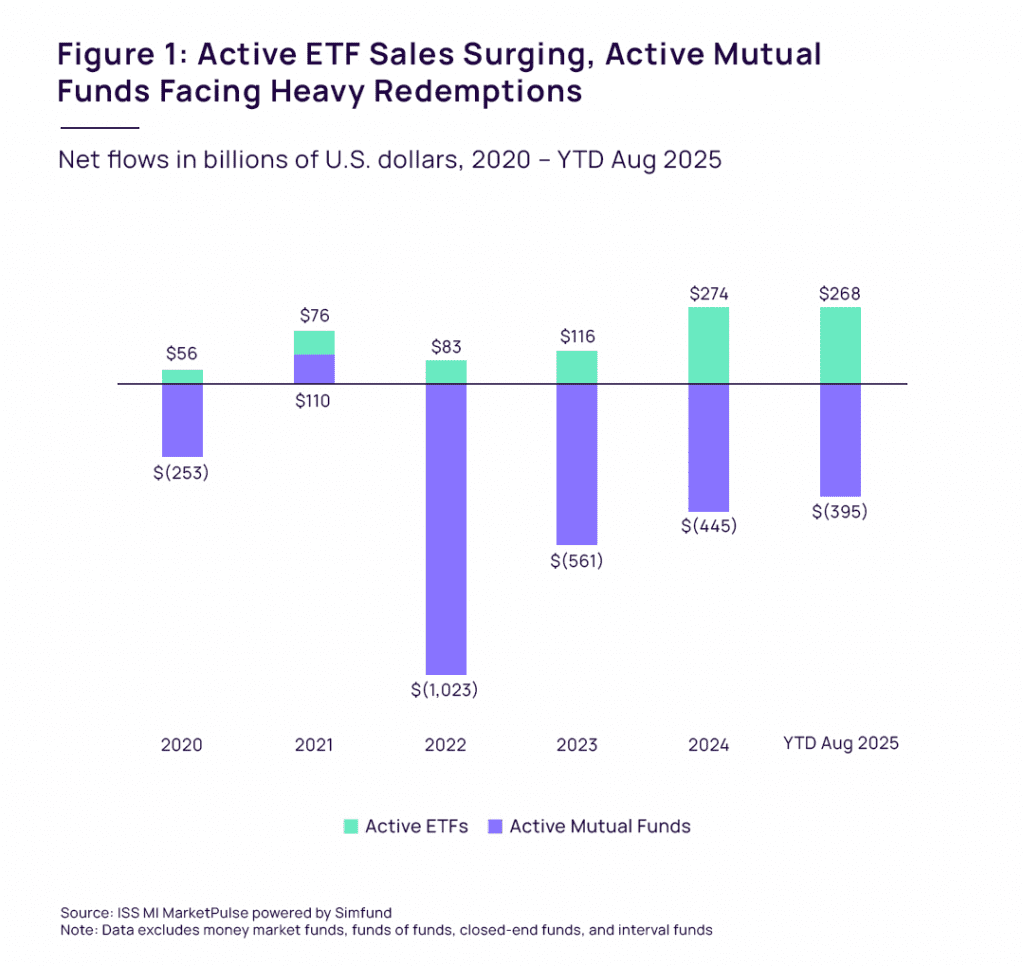

Figure 1 above shows why many asset managers see the SEC’s decision as a win: While active mutual fund sales have been in steep decline, active ETFs have attracted strong interest in recent years. The approved structure offers managers a new route into the fast-growing ETF market—either to capture new sales or to retain existing mutual fund shareholders that might otherwise defect. Launching an ETF from scratch requires building a track record, but a fund with an ETF share class already has one, improving the odds of getting on recommended lists. It also brings the benefit of improved economies of scale.

Certainly, the approval could open vast new ground for ETF investors. The dozens of managers who followed Dimensional’s request for relief in 2023 represent more than half of the active mutual fund market–about $8.5 trillion in assets as of August 2025. (These same players also oversee a further $2.4 trillion in passive mutual fund assets.)

Fund managers are likely to find a receptive audience. Our analysis of institutions’ ETF holdings shows advisors at large wealth managers like LPL Financial and Morgan Stanley have been investing substantial sums in active ETFs. Our survey data also show that advisors increasingly prefer ETFs over other vehicle types; 60% of advisors surveyed by ISS MI in 2024 said they would prefer to access a favored manager in ETF form, versus just 15% for mutual funds. Many flagship strategies still exist only as mutual funds, but that’s likely to change as more funds add ETF share classes. When given a real choice, advisors say they’ll take it.

Advisors may be eager for active ETFs, but they might not get the choice they need to act on those preferences right away. Managers may be reluctant to disrupt an economic model that, despite its challenges, still holds considerable appeal. The shift could also face hurdles from distributors and resistance from investors, especially if the benefits of ETF share classes—like tax efficiency or lower costs—are diluted by operational complexity or strategy constraints. This moment, while potentially defining in retrospect, won’t change everything overnight.

ETF Share Classes for Everyone?

While many managers are eager to launch ETF share classes, the move introduces a new tension: balancing growth with the protection of their existing business. As we wrote in the most recent Windows into Asset Management report, active mutual funds still generate nearly 75% of the fund industry’s revenue, and for some firms, that’s a golden goose worth guarding a little longer.

But the ETF share class structure requires fee alignment across all share classes, leaving managers with higher-fee mutual funds a difficult choice: Cut management fees to make ETF share classes more competitive or maintain pricing and risk losing sales? Managers are likely to resolve this dilemma by rolling out ETF share classes selectively; rather than applying the model across their entire lineups, they will focus on strategies where the economics work and competitive pressure is highest.

Adding ETF share classes to existing mutual funds can also help solve a key distribution challenge faced by stand-alone active ETFs. Some fund platforms have been reluctant to list both a mutual fund and a cheaper active ETF version of the same strategy, fearing regulatory scrutiny. Advisors could be seen as favoring higher-cost options when lower-cost alternatives are available. The ETF share class structure sidesteps this issue by unifying the vehicle under a single fund umbrella.

However, this solution creates new complications. Distributors have spent years streamlining their fund lineups to reduce duplication and complexity. A wave of ETF share class launches could reverse that trend, broadening product shelves distributors have worked hard to trim.

There are also operational hurdles to widespread adoption. Operational differences between ETFs and mutual funds are significant, and most fund providers—including many of those petitioning the SEC for exemptive relief—haven’t yet developed capabilities to manage them. Expect firms with established ETF capabilities to launch ETF classes first.

Unlike mutual funds, ETFs can’t be closed to new investors, which removes a key tool for managing capacity. That makes the structure a poor fit for highly concentrated strategies or those investing in less liquid asset classes, such as small caps or certain fixed income segments.

Will Investors Bite?

Successful products must deliver value not only to fund managers and distributors, but also to end investors. And here is where ETF share classes could face headwinds. The structure still needs to deliver what buyers actually value. If perceived benefits—like tax efficiency—are diluted by the mechanics of mutual fund redemptions, or if the underlying strategy struggles with transparency or capacity constraints, investor enthusiasm may fade.

There’s also a broader skepticism to contend with: many investors believe that pursuing outperformance is a mug’s game, and that most active strategies are likely to underdeliver over time. While the ETF wrapper may improve convenience and reduce fees, it doesn’t change the math all that much. The challenge of consistent active outperformance remains.

By: Christopher Davis, U.S. Head of Research, ISS Market Intelligence