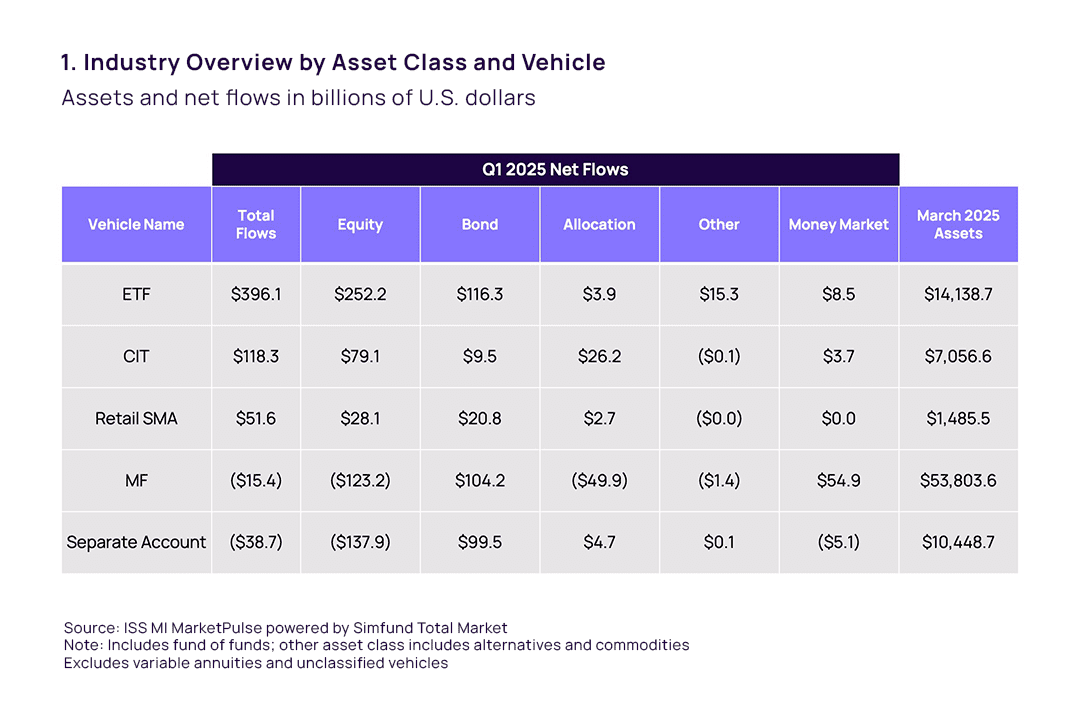

Managed vehicles gathered net inflows of $512.0 billion in Q1 2025, according to data from ISS MI MarketPulse powered by Simfund Total Market. This was the lowest quarter of inflows over the past year and a sizable drop from the $1.0 trillion gathered over the fourth quarter. ETFs led net inflows for the quarter, supported by CITs and retail SMAs.

Industry Overview

ETFs accounted for the largest portion of Q1 inflows by a wide margin. Net deposits totaled $396.1 billion, a slight decline from the $555.8 billion seen in Q4 2024. Passive ETFs continued as the largest contributor to net flows at $276.5 billion, having gathered $452.8 billion the prior quarter. Active ETFs meanwhile grew net inflows from $103.0 billion in Q4 2024 to $119.6 billion in Q1 2025. (For more information on the expansion of active ETFs within the United States, see ISS Market Intelligence’s latest report on Active ETFs and the Expanding Product Shelf.)

Collective investment trusts boosted net commitments to $118.3 billion in Q1 2025 from $58.2 billion in Q4. Allocation products in the form of target-date funds remain a consistent source of inflows, but CIT flows grew in the first quarter primarily thanks to a surge in equity funds. The asset class gathered Q1 inflows of $79.1 billion after $11.2 billion in Q4. Retail separately managed accounts marginally increased net deposits to $51.6 billion in Q1 2025 from $47.3 billion last quarter. Equity funds, predominantly in large-cap strategies, were the leading inflow-gathering segment for the vehicle at $28.1 billion.

Mutual funds had achieved multiple quarters of positive net inflows, though these quarters were dependent on inflows into money market funds. The vehicle fell into net outflows of $15.4 billion in Q1 2025 as flows into money market funds and bond funds lessened from prior quarters. Aggregate net inflows in Q4 2024 had totaled $521.6 billion, with money market funds leading at $527.8 billion.

Institutional separate accounts were the highest source of net outflows at $38.7 billion in Q1 2025. This did, however, serve as a relative improvement from the net redemptions seen in Q4 2024 ($140.1 billion) and Q3 ($138.0 billion). Equity funds faced significant Q1 withdrawals of $137.9 billion, in line with the $140.8 billion of outflows last quarter. Bond funds were the largest source of inflows at $99.5 billion.

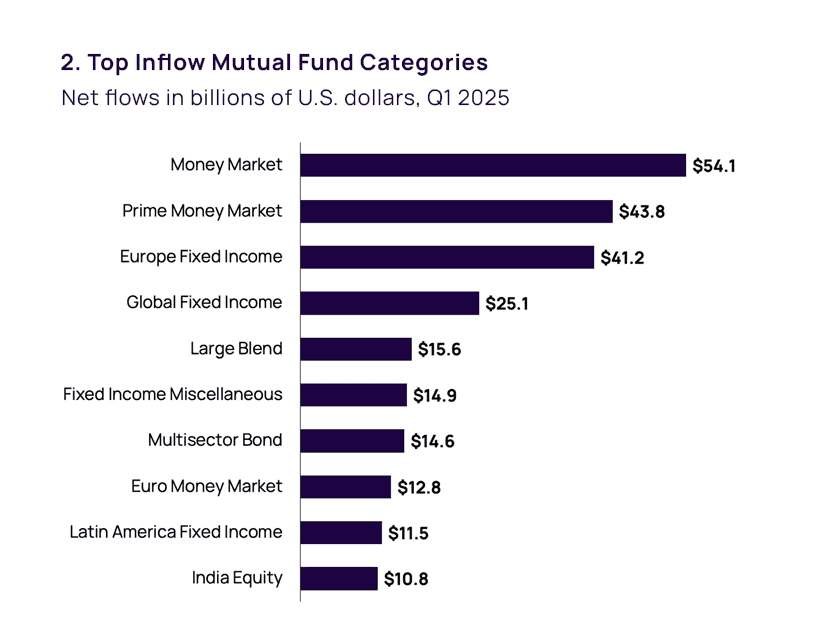

Money market funds remained the largest contributor to mutual fund flows, if at less extensive levels than in recent quarters. U.S. government-focused money market funds led for mutual funds at $54.1 billion, which was a significant drop from the $370.7 billion gathered in Q4 2024. Fidelity was the top inflow-gathering manager in the category at $27.0 billion, followed by Vanguard ($23.8 billion). Prime money market funds followed close behind government funds with net deposits of $43.8 billion, a boost from the $28.9 billion gathered in Q4. Mutual funds saw additional Q1 flows from Euro Money Market funds at $12.8 billion, a decline from the $38.6 billion gathered last quarter.

Fixed income categories ultimately accounted for the highest number of spots on the leading inflow mutual fund rankings at five. Europe Fixed Income led among bond classifications at $41.2 billion, followed by Global Fixed Income ($25.1 billion). CaixaBank was the top-selling Europe Fixed Income manager at $3.9 billion while JPMorgan led for global bond funds at $4.4 billion. European asset managers also led within Fixed Income Miscellaneous through Eurizon Capital ($2.4 billion) and Santander ($1.6 billion). Latin America Fixed Income recorded a rebound from the prior quarter. It had experienced outflows of $24.8 billion in Q4 and grew to inflows of $11.4 billion in Q1, led by Banco do Brasil ($12.2 billion).

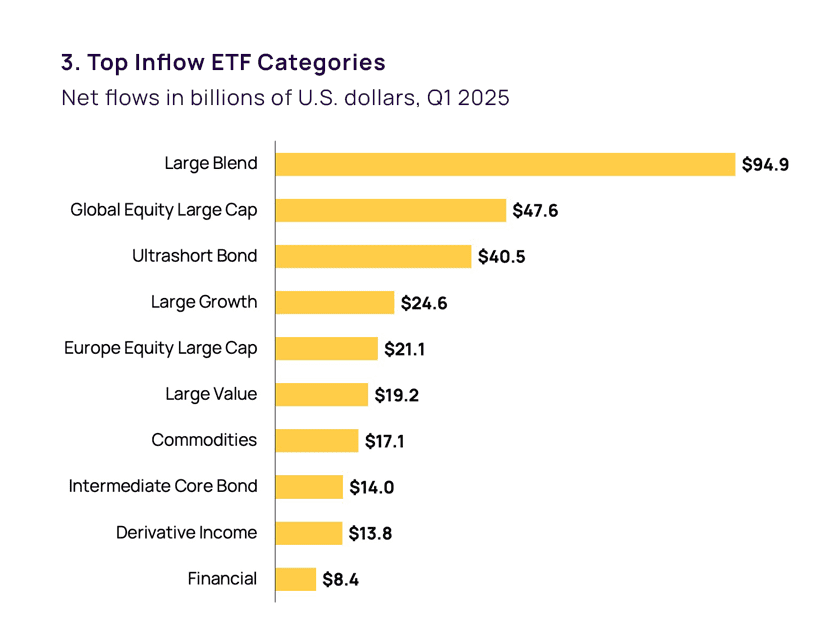

Large-cap equity dominated the list of leading inflow ETF categories, accounting for five of the top six classifications. Large Blend continued as the largest source of inflows at $94.9 billion, though this was half the level recorded in Q4 2024 ($210.1 billion). Passive providers were the primary contributors to the category’s inflows in Q1, with Vanguard gathering net deposits of $50.4 billion and BlackRock seeing inflows of $38.9 billion. Global Equity Large Cap followed with net new flows of $47.6 billion after $59.6 billion in Q4. Large Growth similarly saw Q1 net deposits ($24.6 billion) slightly below Q4 levels ($36.6 billion). Europe Equity Large Cap was the one large-cap category that recorded increased net commitments in Q1, bringing in $21.1 billion after inflows of only $890.0 million in Q4.

Fixed income categories also played a significant role in the quarterly rankings. Ultrashort Bond and Intermediate Core Bond saw much greater representation from active strategies than did the leading equity strategies. Among Ultrashort Bond funds, passive funds gathered inflows of $23.0 billion compared to $17.5 billion from active funds. Index funds accounted for $7.4 billion of Intermediate Core Bond’s quarterly flows, followed close behind by $6.6 billion. Derivative Income was the only category among the top 10 that experienced greater flows into active funds ($12.3 billion) than passive funds ($1.5 billion).

Visit the page next week to see part two, covering retail SMAs, CITs, and separate accounts.

We’re committed to bringing our clients ongoing insights from this expanded dataset and illustrating how this data enables firms to spot opportunities, analyze fund flows across vehicle types, or conduct customized benchmarking. Contact us here or through a Sales or Client Success representative, and visit our MarketPulse site to learn more.

By Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence