Explore Part 1 of Total Market Highlights Q1 2025 for coverage of industry-wide activity and a deeper dive into mutual funds and ETFs.

Managed vehicles gathered net inflows of $512.0 billion in Q1 2025, according to data from Simfund Total Market. This was the lowest quarter of inflows over the past year and a sizable drop from the $1.0 trillion gathered over the fourth quarter. ETFs led net inflows for the quarter, supported by CITs and retail SMAs.

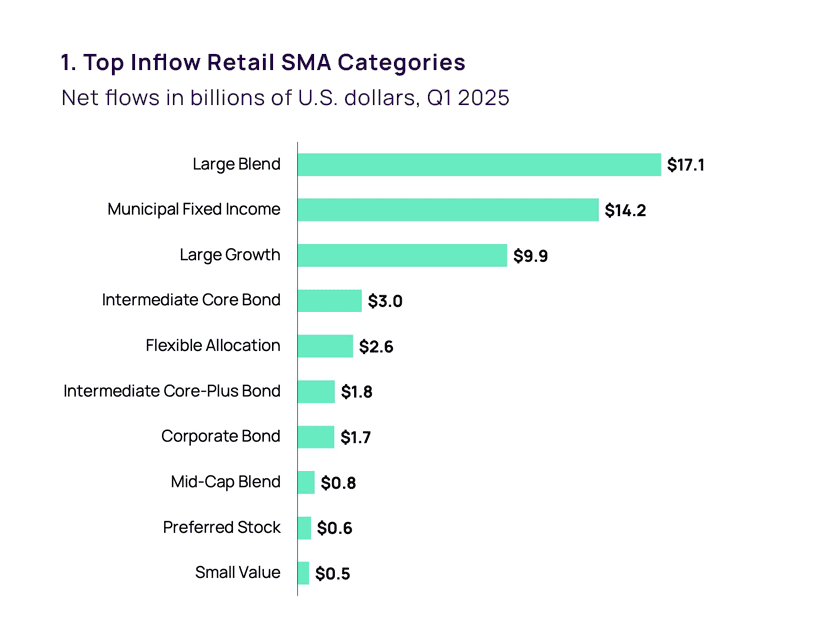

Large Blend acted as the top inflow-gathering category across multiple vehicles in Q1 2025, including retail SMAs, CITs, and ETFs. Among retail SMAs, the category saw marginal improvement in Q1 2025 inflows ($17.1 billion) compared to Q4 2024 ($15.0 billion). In contrast to other vehicles, active strategies garnered greater inflows in Q1 ($10.2 billion) than passive funds did ($6.9 billion). TIAA/Nuveen led in the category at $7.8 billion, followed by Morgan Stanley ($3.9 billion). Within Large Growth, active fund inflows were even more dominant at $9.7 billion compared to $166.5 million for passive funds. JPMorgan was the leading inflow firm for growth funds at $8.7 billion. GQG Partners gathered the second most at $1.6 billion.

The top 10 category rankings also saw representation from multiple bond classifications, though this was strongly concentrated in Municipal Fixed Income. That category gathered inflows of $14.2 billion in Q1, closely in line with the $13.8 billion gathered in Q4 2024. As tax management is a critical use case for SMAs, tax-free bond funds account for a larger portion of ongoing demand within the vehicle than they do elsewhere. The classification saw demand spread across multiple managers in Q1, including Franklin Templeton ($4.7 billion), TIAA/Nuveen ($4.0 billion), and AllianceBernstein ($3.0 billion).

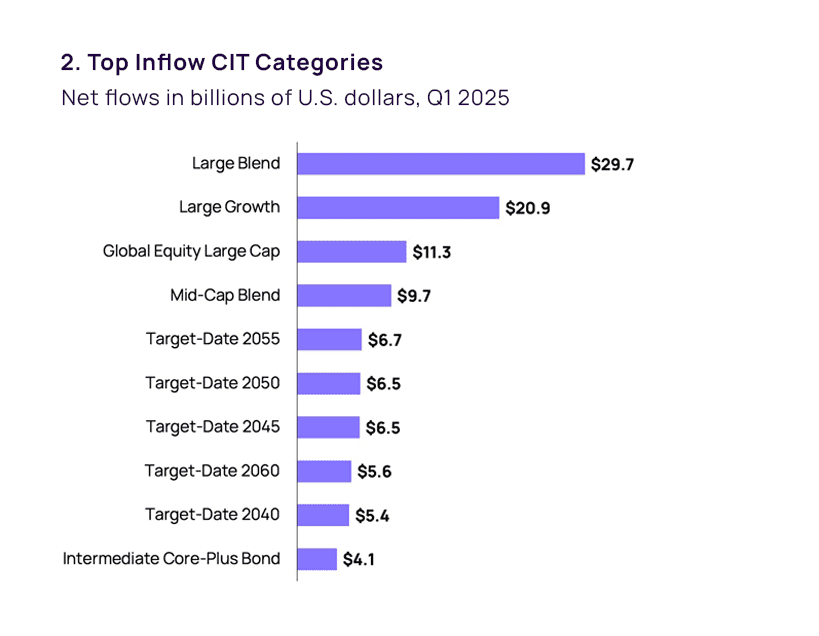

Large-cap exposures served as the largest drivers of CIT inflows as they did among ETFs. Large Blend led net deposits at $29.7 billion, a significant increase from the $6.0 billion gathered in Q4. Large Growth recorded an even stronger turnaround with inflows of $20.9 billion in Q1 after net outflows of $9.8 billion in Q4. Global Equity Large Cap was the only large-cap strategy seeing lower flows in the first quarter ($11.3 billion) than it had in the last quarter of 2024 ($27.1 billion). Index funds were the lead contributor among Large Blend at $25.2 billion, but active funds were the leading segment among growth and global categories. Active funds contributed inflows of $16.6 billion to Large Growth and $18.1 billion for Global Equity Large Cap.

The central role that CITs play within retirement plans leads to extensive representation from target-date strategies, which accounted for half of the leading inflow categories. Target-date categories collectively gathered inflows of $26.9 billion over the first quarter, below the $41.5 billion brought in during Q4. Vanguard experienced the highest level of flows across all target-date classifications at $14.4 billion. Capital Group and Fidelity witnessed the next highest inflows at $11.7 billion and $4.0 billion, respectively. (Click here for more information on the increasingly large role CITs play within retirement plans, as covered within ISS MI’s Windows into Defined Contribution report and other Total Market reports.)

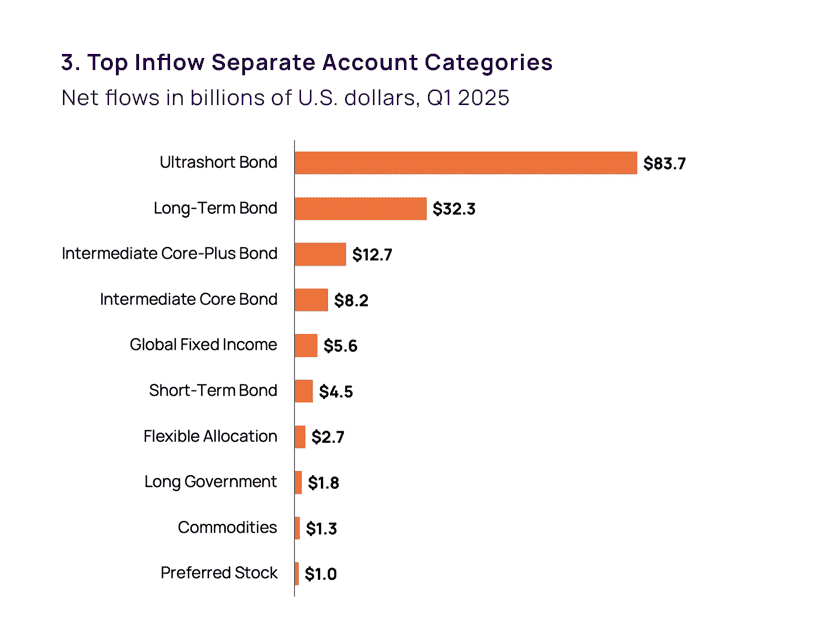

Fixed income groupings overwhelmingly led the top inflow rankings for institutional separate accounts, accounting for the top six categories and contributing aggregate net inflows of $99.5 billion. Demand was particularly concentrated in Ultrashort Bond. The category gathered inflows of $83.7 billion in Q1 2025, an exceptional boost from the $9.2 billion seen over Q4 2024. Multiple other bond categories experienced significant boosts in net flows compared to the prior quarter. Long-Term Bond, for example, recorded net deposits of $32.3 billion after only $27.3 million in Q4. Intermediate strategies experienced sizable rebounds from Q4, when core-plus strategies saw outflows of $10.3 billion and core funds faced net redemptions of $7.5 billion. Short-Term Bond and Long Government were the only bond classifications that saw lower inflows than they had in Q4 at $6.1 billion and $4.0 billion, respectively.

Equity categories saw significant aggregate outflows from separate accounts in Q1 of $137.9 billion. Outside of bond categories, allocation and commodity funds recorded minor inflows. Flexible Allocation saw net deposits of $2.7 billion for the quarter, rebounding from Q4 outflows of $2.5 billion. PIMCO led in the category in Q1 at $3.7 billion. Commodities gathered $1.3 billion in Q1, also led by PIMCO at $993.7 million.

We’re committed to bringing our clients ongoing insights from this expanded dataset and illustrating how this data enables firms to spot opportunities, analyze fund flows across vehicle types, or conduct customized benchmarking. Contact us here or through a Sales or Client Success representative, and visit our MarketPulse site to learn more.

By Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence