Exchange-traded funds (ETFs) are taking on an increasingly central role within the asset management industry. Passive ETFs dominate total inflows while active ETFs experience rapid growth and serve as the primary vector for new active demand. As asset managers work to gain investors’ attention in a progressively more competitive market, understanding where to focus resources becomes a critical step to success in the ETF market. New data within ISS MI’s MarketPulse reveals the leading owners of ETFs, allowing asset managers to target the most promising opportunities.

ISS MI has helped financial institutions better understand trends in product development, burgeoning asset classes and strategies, and the shifting fee landscape. The addition of data from 13F filings into MarketPulse ties historical assets and flows of ETFs held by intermediaries to other product characteristics, including categories, performance, and fees, helping product manufacturers enhance their distribution strategies. (Form 13F is a quarterly report filed with the SEC by investment managers and registered investment advisors who oversee at least $100 million in eligible securities, including equities, options, and ETFs.)

MarketPulse data employing 13F filings captured nearly $7 trillion in ETF assets as of June 2025. Passive ETFs accounted for the largest portion by a wide margin at $6.1 trillion in June. Active ETF growth has nonetheless been exceptionally strong in recent years, with 13F filings capturing assets of $747.1 billion as of June. Previous ISS MI research on 13F filings discussed the extensive role that RIAs and fee-based advisors played in adopting ETFs.

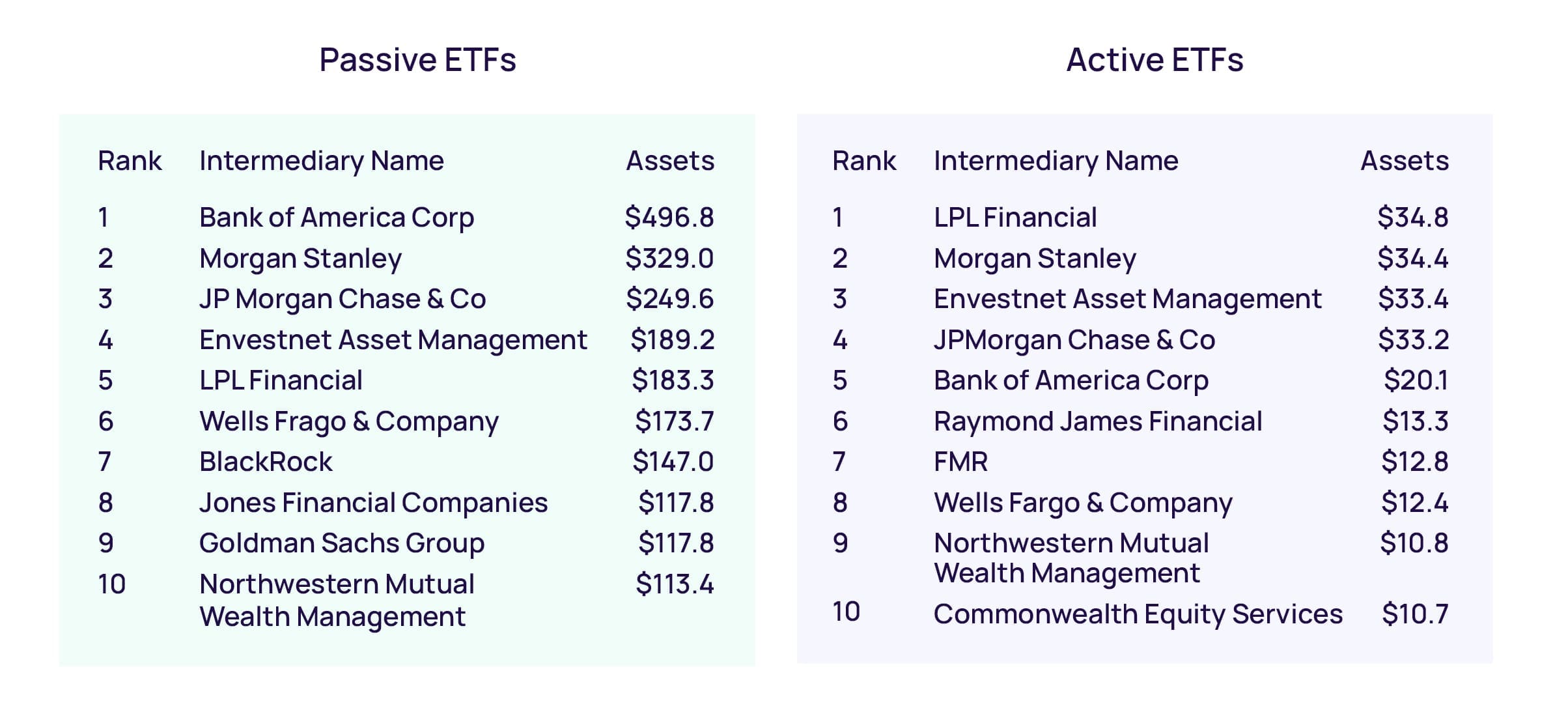

Leading fund distributors have all committed extensively to the use of ETFs. Figure 1 displays the top holders of passive and active ETFs. While the rankings of the largest passive ETF and active ETF users saw significant overlap, active ETFs demonstrated relatively more acceptance among independent channels. LPL Financial stood out as the top user of active ETFs in Q2 2025.

1. Leading Distributors Commit to ETFs

ETF assets in billions of U.S. dollars by intermediary distributor, June 2025

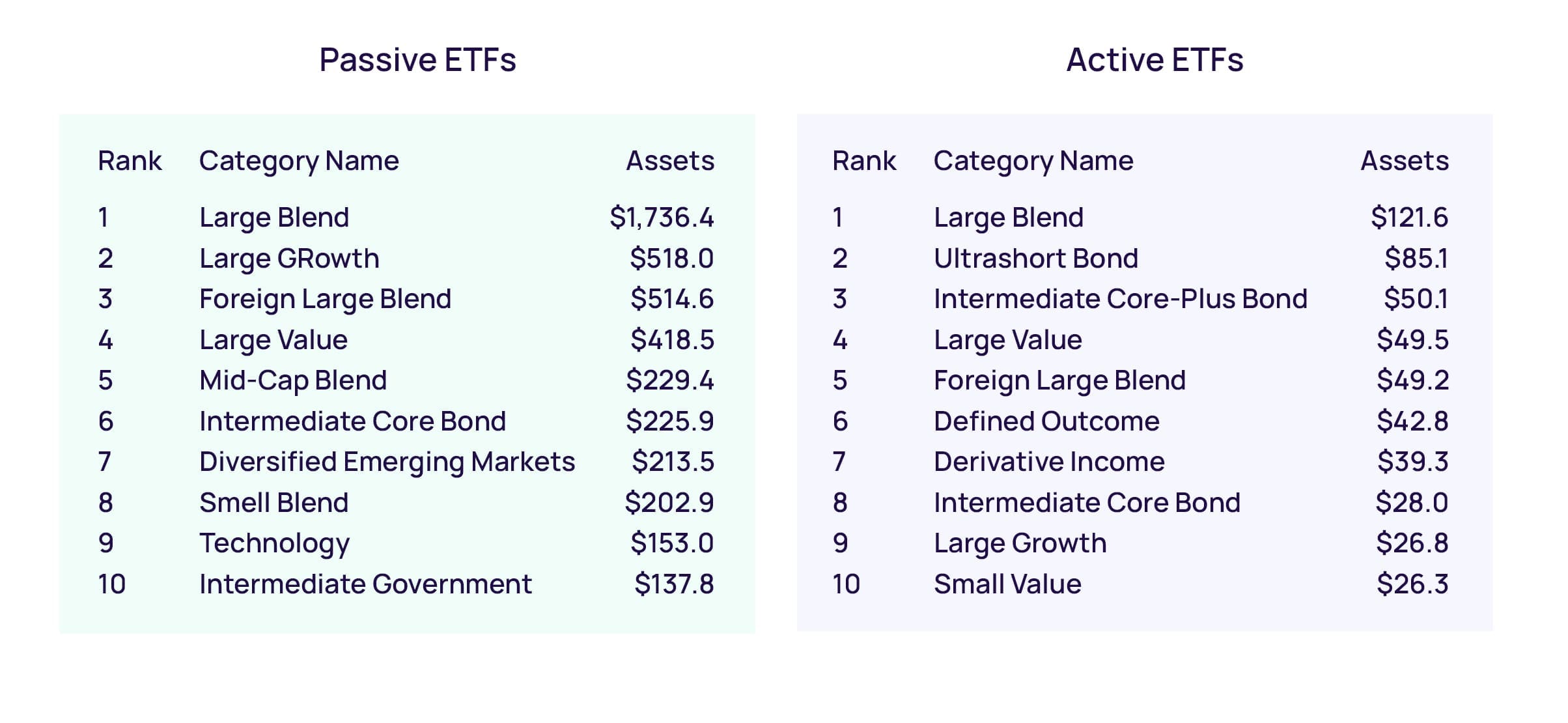

Large Blend, which contains leading funds like the Vanguard S&P 500 ETF and SPDR S&P 500 ETF, is the largest strategy across passive and active ETFs. Its dominance is similarly reflected in the list of leading strategies held by 13F filers. Among passive ETFs, the category has a $1 trillion lead over the next largest category, Large Growth. Large-cap equity strategies ultimately account for four out of the five largest categories for index ETFs.

Active ETFs have demonstrated greater diversity in their largest strategies. While Large Blend still leads among active ETFs, it is with a much smaller lead than among passive funds, as seen in Figure 2. Advisors using active ETFs have used them more extensively in fixed income and non-traditional strategies. The vehicle started out as one strongly associated with Ultrashort Bond funds, which has persisted amidst an uncertain interest rate environment. Categories like Intermediate Core-Plus Bond, Large Value, and Foreign Large Blend experienced higher relative adoption among intermediary players than they did within the broader active ETF universe, highlighting how important active management are for advisors as they seek out areas where liquidity constraints and informational asymmetries create opportunities to generate alpha. ISS MI’s surveys with advisors have similarly found active management as a core reason for advisors to pick active ETFs, with 44% of advisors in the 2024 Advisor Pulse on vehicle preferences listing it as a top three reason for choosing the vehicle.

2. Large Blend Dominates ETF Holdings, Active Funds See Greater Bond and Alt Representation

ETF assets held by 13F filters in billions of U.S. dollars by category, June 2025

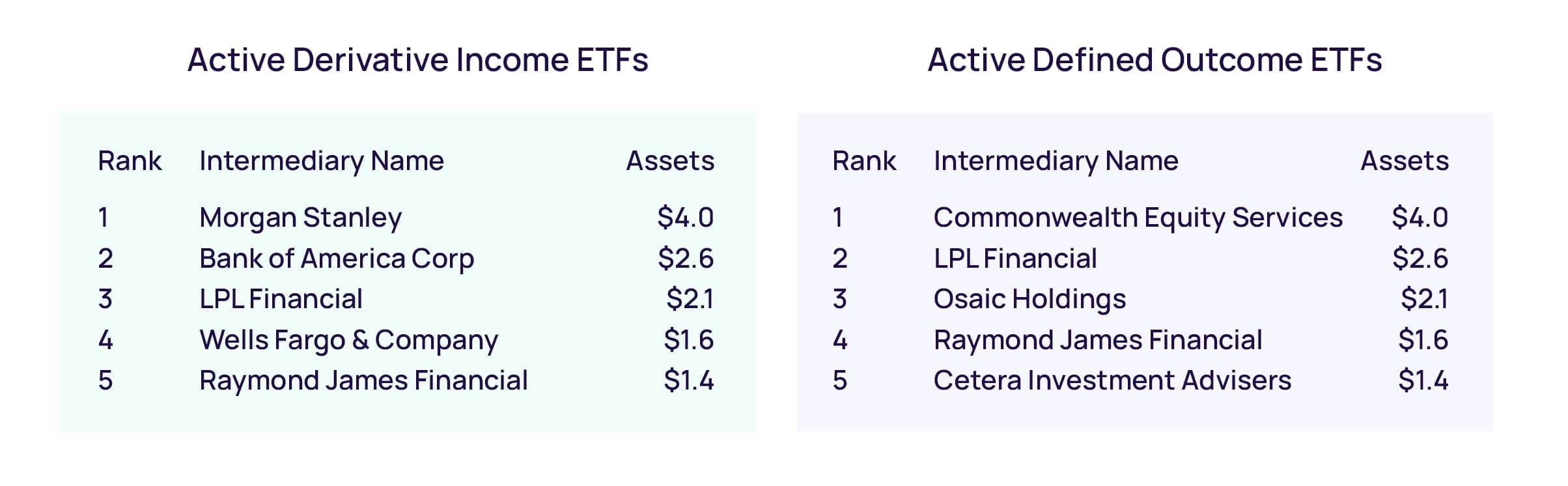

Active ETFs have grown through managers offering variants of popular strategies as well as converting existing strategies from mutual funds into ETFs. More importantly for active managers looking to enter or expand within the market, funds launched in recent years have accounted for the largest portion of growth within active ETFs as covered in ISS MI’s recent Active ETFs and the Expanding Product Shelf. Defined Outcome and Derivative Income are examples of strategies that saw their most significant debuts after 2020 and have achieved significant investor adoption. Both strategies employ options and other derivatives alongside equity exposure and seek to either protect against market declines (Defined Outcome) or generate additional income (Derivative Income).

3. Alternative Active ETFs See Diverse Adoption

Alternative active ETF assets in billions of U.S. dollars by intermediary distributor, June 2025

The different approach that the categories take in their use of derivatives has subsequently led to a stark difference in adoption by distributors. Wirehouses, including Morgan Stanley, Bank of America, and Wells Fargo, have served as leading adopters of derivative income funds, as seen in Figure 3. Defined Outcome funds, conversely, were more popular among independent broker-dealer advisors and RIAs.

Even among vehicles within the same asset class, advisors may have starkly different approaches about what best works for them and their client base. MarketPulse enables comprehensive market analysis by tracking ETFs and their owners across multiple dimensions, creating a truly unique strategic intelligence platform that benefits both product and distribution teams. For more information on the inclusion of 13F data in MarketPulse, contact us here or through a Sales or Client Success representative, or visit our MarketPulse site to learn more.

By Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence