“Forecasting is very difficult, especially when it involves the future.” – Yogi Berra

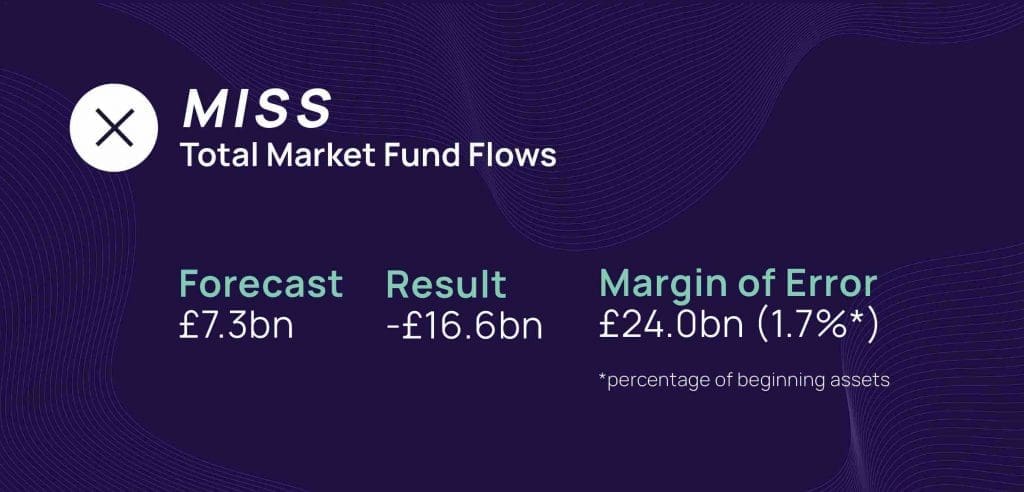

Reviewing one’s fund flow forecast[1] is not for the faint of heart, as investor sentiment can change on a dime. That appears to have happened with our forecast for June to November’s UK-domiciled fund flows. The period between December 2022 and May 2023 ended on an optimistic note, with May flows positive to the tune of 0.3% of beginning assets—a result that likely tilted our forecast towards predicting slightly positive flows in the months ahead. That, however, would not come to pass. Flows have been negative in every month since May. Indeed, the six-month flows ending November 2023 showed net outflows of 1.2% of beginning assets, or 1.7% below our original prediction.

The miss would not hurt so much, except that for three of the four long-term asset classes predicted, an overestimate of fund flows was made. However, these misses are hardly surprising. In addition to seeing red continually flash within the Simfund dataset, fund flows have also consistently flashed red within the retail channels captured through ISS MI’s Financial Clarity dataset.[2] Given this challenging environment, opportunities have been harder to uncover. One has often had to pull out their magnifying glass to see them.

Not As Bo(u)nd for Success As Imagined

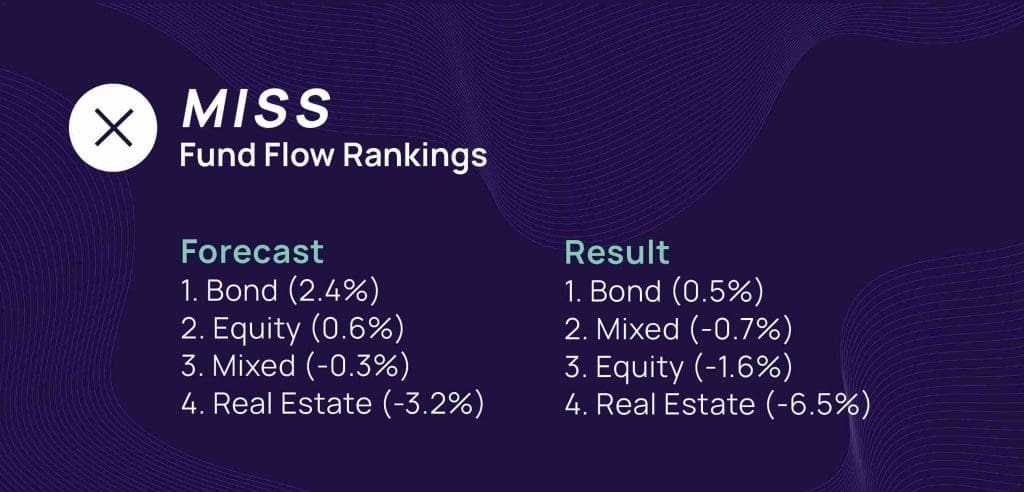

Bond funds were anticipated to generate the greatest amount of fund flows, which is exactly what happened. Flows into bonds, however, were much more muted (0.5% of beginning assets) than anticipated (2.4% of beginning assets). Rising—and particularly potentially peaking rates—have certainly increased investor interest in fixed income products, though that attention has yet to materialize into significant flows. Looking at fixed income beyond bond funds, it is notable that financial institutions’ sterling deposits from household sectors increased.[3] It is therefore reasonable to assume that higher deposit rates are putting some downward pressure on bond fund sales. The impact of higher money market rates was less transparent. Sterling denominated money market funds saw outflows during this period. It is possible though that UK investors chose other money market denominations in funds domiciled outside the UK.

What did sell over the six months covered were GBP government bond, global bond, and global corporate bond funds. For both the GBP government bond and global bond categories, flows were primarily driven by passive funds. Passive funds now account for nearly two-thirds of assets in both categories. Active bond fund managers therefore have their work cut out for them and may increasingly be relying on high-yield and corporate bonds to drive their fund sales figures higher. While the window for bond funds is far from closing, investor preferences may become telling if greater action, in the form of increased positive flows, is not witnessed soon.

Mixed funds, mixed results

While the mixed bag metaphor is likely getting tired, it continues to aptly describe the fund flow experience for the mixed asset class. Our relatively modest prediction of 0.3% in net outflows ended up being spot on, with net outflows coming in at an estimated 0.7% of beginning assets.

Behind this figure, however, was a continued divergence in the fate of mixed funds with a target equity weighting above or below 60%. Mixed funds with an equity share above 60% achieved modest net inflows of over £3.5 billion, while those under the 60% mark saw net outflows topping £6.0 billion. The main winners from this trend were True Potential and BlackRock. Whereas True Potential saw several growth-oriented funds generate positive flows, BlackRock’s flows were largely driven by several institutionally focused funds launched since November 2022. Previously, we postulated that conservative funds would gain steam in line with bond funds, so until that comes true, do not expect a turnaround in these funds’ fortunes.

Investors voting with their wallets when it comes to the UK

The equity forecast missed by £18.2 billion on the downside; £11.4 billion of that was down to UK equity funds experiencing far greater outflows than expected. Until the UK equity market improves, however, it is anyone’s guess as to how far this downward trend in flows will continue. It is notable, however (and a topic that will be explored in a future paper) that most European domiciles are seeing an exodus from domestic equity—major equity index performance, notwithstanding.

The next most significant miss was on global equity (£7.2 billion), where flows turned negative in direct opposition to the positive flows forecast. Whereas global funds were predicted to retain their winning streak, it turned out that investors preferred Asian equity and US equity funds. In fact, US equity fund flows beat their forecast, the only sub-category outside of the mixed asset class to do so. Equity flows are expected to continue to mimic or trail equity market performance, and as long as U.S. markets—largely driven by the Magnificent Seven stocks—outperform, expect investors to follow. Outside the United States, Japanese equity was the hottest commodity.

For sale: Property funds continue to exit

In the previous forecast, daily traded direct property funds were anticipated to be in for a rough ride. Since that last forecast, St. James Place, M&G Investments and Canada Life Asset Management have closed property funds, and direct property funds, particularly with the latest wave of closures, remain challenged to find new investors. However, there is hope that the long-term asset fund (LTAF) structure and a more flexible allowance around withdrawal periods can rejuvenate this asset class. Certainly, this is the least surprising miss of the many misses this time around.

“Oft hope is born when all is forlorn.” – JRR Tolkien

The second half of 2023 continued to be a challenging period in which to market and sell investment funds; just one single fund manager generated net inflows above £2 billion through their UK-domiciled fund lineup. On the surface then the picture looked bereft of opportunity. Look deeper though, and opportunity begins to present itself.

Opportunity remained for passive funds and could be seen at the sub-asset class level. Additionally, the Financial Clarity dataset continues to highlight the opportunity for fund managers to drive flows through being included in model portfolios. Flows into models have been positive throughout 2023. Finally—and representing a future opportunity—the Financial Conduct Authority’s (FCA) Sustainable Disclosure Regime, which will bring in four new fund labels. These three opportunities have one thing in common: all require adapting to a new reality—a reality in which value and the transparent demonstration of this value to clients and advisers is paramount.

Today’s economic environment remains a challenging one—a circumstance that will certainly change. While the base needs of investors will remain, how these needs are met, whether in terms of asset class or product type, may not. Certainly, now is the time to prepare for tomorrow, for the investment taps will flow again. The question is whether investment funds will be able to refill their buckets next time around.

Explore how Simfund and Flowspring can help you forecast future fund flows, and learn more about ISS Market Intelligence.

Notes:

[1] Forecasts have been produced using data from ISS MI’s Flowspring and Simfund products

[2] For further details on the IFA channel in Q3, please check out: https://insights.issgovernance.com/posts/when-it-rains-it-pours-q3-2023-financial-adviser-sales-highlights/

[3] For more details, check out the Bank of England’s Monthly changes of monetary financial institutions’ sterling retail deposits (excluding notes and coin) from household sector (in sterling millions) not seasonally adjusted data series

Commentary by ISS Market Intelligence

By: Benjamin Reed-Hurwitz, Vice President, EMEA Research Leader, ISS Market Intelligence