Read part two, covering total market flows, ETFs, and mutual funds.

Managed vehicles recorded net inflows of $1.1 trillion in Q4 2025, according to data from ISS MarketPulse powered by Simfund Total Market. This represented a notable increase from the $885.0 billion raised in the third quarter as well as the highest quarterly total in four years. Net deposits for 2025 overall totaled $3.2 trillion, a slight decrease from the $3.4 trillion gathered during 2024.

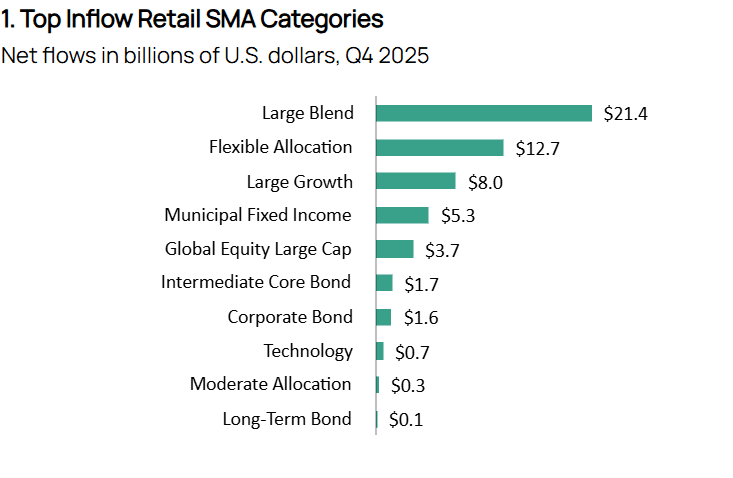

Retail SMA categories closed Q4 with net commitments of $51.1 billion, effectively in line with Q3’s $52.0 billion. The top rankings included four fixed income categories, four equity strategies (three of which were large-cap), and two allocation categories. Large Blend led the pack with net deposits of $21.4 billion, up from the $12.7 billion seen in Q3. Other large-cap equity strategies also improved, with Large Growth ($8.0 billion) and Global Equity Large Cap ($3.7 billion) both seeing increased flows compared to Q3. Technology saw a modest dip in Q4 with $741.4 million inflows compared with $835.2 million in Q3. Municipal Fixed income typically plays a key role within retail SMA flows due to the structure’s extensive use for tax-managed strategies. The category continued with positive demand of $5.3 billion in Q4, though this was well below the $13.1 billion recorded in Q3.

For coverage of industry-wide activity and a deeper dive into mutual funds and ETFs, read our blog post: ETF, MF, and CIT Flows Surpass $1 Trillion in Q4 2025.

Allocation strategies were the second largest net contributor to SMA flows on an asset class level. Flexible Allocation saw the second highest inflows at $12.7 billion, a sharp rise from $9.4 billion in the prior quarter. Moderate Allocation also added $332.6 million in net inflows. Among SMA managers overall, BlackRock gathered the highest inflows at $27.3 billion. The firm accounted for majority of Q4 demand in Large Blend ($13.2 billion) and Flexible Allocation ($12.5 billion). JPMorgan followed as the next highest inflow manager at $8.8 billion, driven by Large Growth ($6.8 billion).

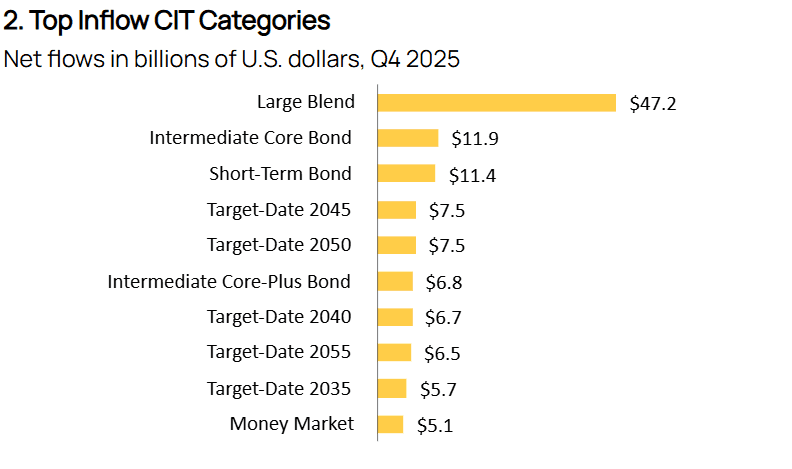

Large Blend served as the top CIT inflow category in Q4 2025, attracting $47.2 billion, a sharp increase from $4.2 billion in Q3. The surge was driven by a significant rebound in passive fund activity, with passive strategies drawing $44.8 billion, compared with $2.5 billion in outflows in the prior quarter. Vanguard led the Large Blend category with $19.0 billion in net commitments, a jump from $12.9 billion seen in Q3, while Northern Trust followed with $11.9 billion, marking a strong turnaround from $989.6 million in prior quarter outflows. Geode Capital Management acted as the third highest inflow manager with $11.6 billion inflows, up moderately from $8.9 billion in Q3. All three firms saw their net deposits primarily through passive S&P 500 products. Fixed income categories also contributed meaningfully, supported by broad improvement from Q3. Intermediate Core Bond, for example, grew net inflows from $7.2 billion in Q3 to $11.9 billion in Q4. Short-Term Bond saw an even stronger recovery from Q3 outflows of $1.3 billion to Q4 net commitments of $11.4 billion. Intermediate Core-Plus Bond also improved from Q3 inflows of $1.3 billion to Q4 inflows of $6.8 billion.

Target-date categories accounted for five of the leading inflow CIT groupings in Q4, reflecting their central role in defined contribution retirement plans. Net flows into all target-date CITs totaled $42.9 billion for the quarter, though this was down from $53.4 billion in Q3. Fidelity Investments led the segment with $9.8 billion in inflows, followed by Capital Group at $9.3 billion.

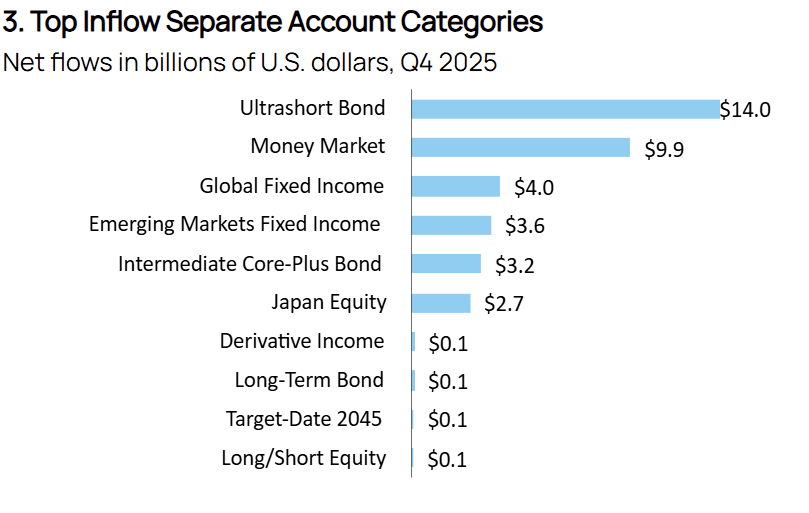

Fixed income continued to dominate institutional separate account inflows in Q4, accounting for five of the top ten categories. Ultrashort Bond led the category with $14.0 billion, much sharper than $3.2 billion in Q3. JPMorgan drove most of the Q4 activity at $7.4 billion. Global Fixed Income ranked third with $4.0 billion in inflows, down from $9.5 billion in the prior quarter. Inflows from other bond categories saw a strong turnaround with Emerging Markets Fixed Income ($3.6 billion), Intermediate Core-Plus Bond ($3.2 billion), and Long-Term Bond ($131.4 million) all reversing the outflows that they saw in Q3. A more conservative and risk-off approach echoed throughout other asset classes in institutional separate accounts. Money Market saw the second highest inflows at $9.9 billion in Q4, a stark reversal from Q3’s outflows of $440.4 million.

Net flows into other categories were comparatively meager. Japan Equity made it to top ten categories with $2.7 billion in flows, after $744.7 million in Q3, but no other category experienced net inflows above $150 million. Among these lower inflow categories, Long-Term Bond recorded the most improvement from outflows of $11.1 billion in Q3 to minor inflows of $131.4 billion in Q4.

We’re committed to bringing our clients ongoing insights from this expanded dataset and illustrating how this data enables firms to spot opportunities, analyze fund flows across vehicle types, or conduct customized benchmarking. Contact us here or through a Sales or Client Success representative, and visit our MarketPulse site to learn more.

Authors:

Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence

Antara Maity, Senior Associate, U.S. Fund Research, ISS Market Intelligence

Aishwarya Mahalingam, Associate, U.S. Fund Research, ISS Market Intelligence