Advisors intend to increase their usage of direct indexing

The aggressive growth of passive investment has been an inescapable trend for managers in the investment industry. The relentless pressure on fees drives down costs while potentially concentrating assets among the top players who can best use their scale to further reduce costs. Direct indexing, in which investors directly hold the securities that make up an index rather than invest in shares of a fund, has served as one way for investment managers to participate in the growing demand for passive investing while offering additional customization opportunities for clients.

ISS Market Intelligence explored advisor sentiment around direct indexing, in addition to trends around vehicle preferences and portfolio construction, in the September edition of its ISS MI Advisor Pulse Series, which surveyed 806 advisors in July 2024. ISS MI’s surveys found significant future interest in the approach. When advisors were asked whether they intended to increase or decrease usage of specific vehicles over the next twelve months, direct indexing had the second highest net future increase of any vehicle at 38%, behind only active ETFs (53%).

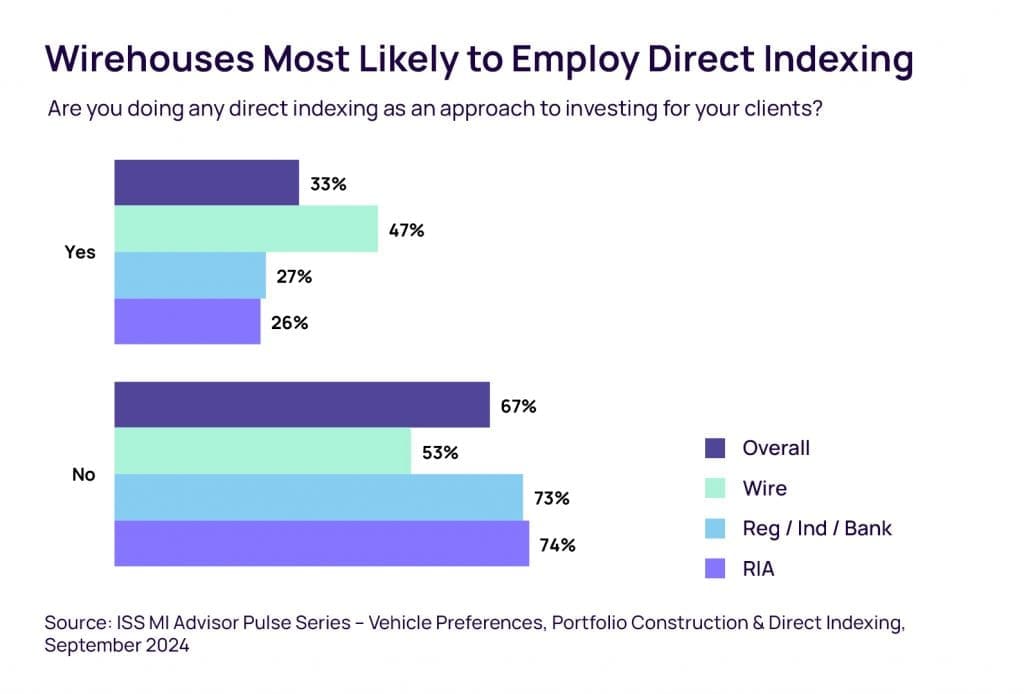

Wirehouse advisors are the most likely to use direct indexing

This sizeable increase in the usage of direct indexing comes partially from the fact that the approach is coming from a small base and is still working to gain adherents. Nearly two-thirds of advisors stated that they do not currently use direct indexing with clients, as seen in the chart below. Wirehouse advisors were the most likely to reference using it at 47%.

Direct indexing likely resonates with wirehouse advisors because it is an approach designed for ultra-high-net-worth clients that are most frequently found in the channel. Private alternatives have been most popular within the channel for similar reasons. Alternatives differ strongly from direct indexing, in that the former aims for uncorrelated returns and features high management fees whereas the latter seeks out low-cost market beta, but both require substantial investment minimums. In the case of direct indexing, large asset pools are necessary to make it competitive with the cost of a traditional index fund.

Greater control over tax management strategies is seen as the leading benefit of direct indexing

In line with the appeal to wealthier clients, advisors interested in direct indexing were most likely to cite its benefits for tax management. When asked about the top benefits of direct indexing, 40% of advisors referenced its greater control over tax management strategies as the leading benefit, followed by 27% that said it helps them tailor investments to satisfy specific client needs. These needs might include, for example, a client employed by a leading tech firm. That client will already be heavily exposed to changing conditions in their employer through their paycheck and potential stock options. Direct indexing allows that client to exclude that firm’s securities from their index holdings. While the approach still has room to go in winning over converts, its appeal to wealthy clients will continue to generate interest from asset managers and advisors.

Six times each year, ISS Market Intelligence (ISS MI) surveys Advisors across the country to understand the advisor decision making process and their perceptions of firms across the asset management industry. Download a Summary of the latest issue of the Advisor Pulse research series.

Alan Hess, Vice President, ISS Market Intelligence