Launch activity remained elevated in the first quarter of 2026, driven largely by ETFs, even as closures continued at a steady pace. This is not a market pulling back, but one actively testing ideas and moving quickly to determine which products merit staying power.

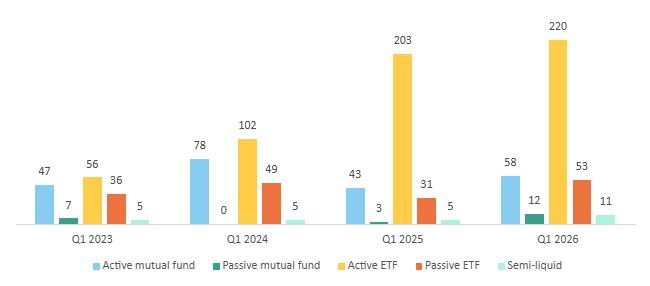

Active ETFs continued to anchor launch activity. The quarter saw 220 launches, slightly ahead of Q1 2025’s pace. Considering that 2025 as a whole saw nearly 1,000 new active ETFs, 2026 stands to be another year of extremely high product development. Active ETF issuance has settled into a structurally elevated range, highlighting how fully the wrapper has been integrated into managers’ core product strategies.

Importantly, this activity extends far beyond simple repackaging. Even excluding conversions, 202 new active ETFs launched during the quarter, highlighting firms’ continued willingness to seed fresh strategies.

Active ETFs See Record Q1 Launches

Source: ISS MI MarketPulse powered by Simfund.

Mutual fund-to-ETF conversions nonetheless played a more meaningful role in Q1 2026 than in prior first quarters. Over the period, 18 active mutual funds transitioned into ETFs, more than double the total in Q1 2025. The interest in conversions has accelerated even as other venues for fund transformation have opened up. More than 100 asset managers have applied for exemptive relief to attach ETF share classes to their existing mutual funds, with roughly 70 approvals granted to date.

Three firms have already launched dual-share structures, which can be tracked using the new “Dual-Shares Fund” flag in ISS MI MarketPulse.

ETFs are increasingly being deployed alongside traditional vehicles, and in some cases positioned to supplant them, as firms reassess how best to deliver and preserve strategies. The shift is also evident in where launches are concentrating. Defined outcome, single-stock, and derivative income ETFs continue to lead, reflecting strategies that are purpose-built for the ETF format.

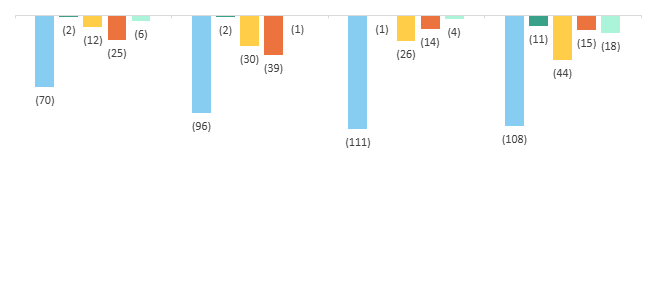

Outside the ETF universe, activity was more varied but still constructive. Active mutual fund launches increased to 58 from 43 a year earlier, while passive mutual fund launches rose to 12. Semi-liquid fund launches reached 11, matching prior highs; interval and tender‑offer funds gained traction as interest in hybrid liquidity structures persisted. That momentum continues to be matched by decisive consolidation. Active mutual fund liquidations and mergers totaled 108 during the quarter, while active ETF closures rose to 44, the highest first quarter total on record. Firms remain willing to experiment, but increasingly quick to prune underperforming ideas.

Overall, Q1 suggests an industry not slowing down, but becoming more focused. Innovation remains alive and well, ETFs continue to drive the product launch conversation, and consolidation has become more far reaching. For the remainder of 2026, success will depend less on the number of launches and more on whether certain products prove resilient enough to earn staying power.

Talk to us today about how ISS Market Intelligence can help your business.

Authors:

Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence

Antara Maity, Senior Associate, U.S. Fund Research, ISS Market Intelligence