Alternative managers hope to enter the DC market

Stakeholders across the asset management industry have taken great interest in alternative strategies in recent years. Traditional managers have sought to acquire or partner with alternative specialists who themselves want access to wider pools of investors. Wealth managers, meanwhile, are on the lookout for strategies to satisfy high-net-worth clients.

Defined contribution (DC) markets, however, are one segment that has proven historically resistant to alternative adoption. While defined benefit (DB) plans have long been users of alternatives, DC plans have fewer liquid or illiquid alternative strategies. A concerted push by alternative managers and potential shifts in regulation could open new ground in retirement plans, but in order for this to succeed, the DC market will likely require much firmer guidance and more definitive changes in regulation.

Slim past

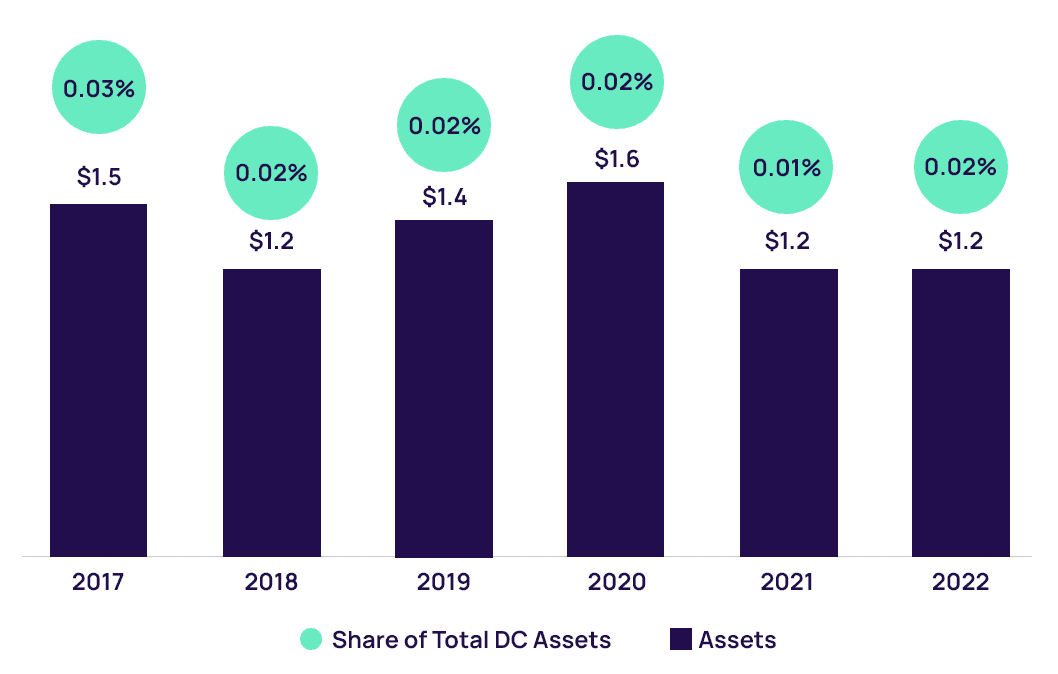

DC markets have historically been less likely to adopt the newest product trends as a result of a slower and more deliberate approach on behalf of their less financially engaged investors. While the liquid alternative strategies that came to market more than 15 years ago would have met the liquidity and reporting requirements of other DC options, they experienced little uptake from retirement plans. The short records of many such strategies, the lack of familiarity many investors had with either liquid or illiquid alternatives, and sponsor concerns about liability served to hamper adoption. Figure 1 below displays data over time on standalone alternative strategies within DC plans according to Form 5500 data gathered by ISS MI MarketPro Retirement. The $1.2 billion held in alternative strategies as of the end of 2022 is a far cry from the more than $7 trillion in assets those plans held that year, according to ISS MI data.

Figure 1: Alternative Options See Minimal Presence on DC Plans

Assets of standalone alternative options on DC plans in billions of U.S. dollars, 2017 – 2022

Liquid alternatives faced difficulty from their inception, landing on DC plan line-ups. They began to face more headwinds overall in the registered market across 2015 and 2016 due to continued hurdles with investor education and the perception that liquidity requirements robbed liquid alternatives of their alpha potential. Over the past decade, asset managers’ interest in alternatives has focused more extensively on private, illiquid, and semi-liquid options.

Managers seeking to expand into DC plans have also been examining private strategies. A significant move in incorporating these strategies occurred during the first Trump administration. In response to a request for clarity from Pantheon Ventures and Partners Group, the Department of Labor (DOL) opened the path for alternatives sleeves within registered funds by stating in June 2020 that “…a plan fiduciary of an individual account plan may offer an asset allocation fund with a private equity component […] in a manner consistent with the requirements of Title I of ERISA.” The letter acknowledged the differences between DC and DB plans in their abilities to evaluate these options and the complexity, long time, and higher fees of private equity (PE) investments, stressing that plan fiduciaries needed to evaluate the risks and benefits of this approach.

A promising but uncertain future

Certainly, the historically litigious nature of the DC market creates complications for any expansion of alternatives— the very features that render them of interest to asset managers could encourage potential litigants to target them. One reason alternatives can command higher fees is that they offer return streams not easily available elsewhere. These non-traditional strategies also come with much higher dispersions in returns. The difference between top and bottom quintile performers is much wider in less regulated and less efficient strategies like private equity and private credit than it is for the more extensively covered large-cap equity space. Participants have already demonstrated a willingness to engage in litigation over relatively small differences in performance in plan line-ups. Incorporating alternatives into other strategies, such as target-date funds, may well prove crucial to overcoming the scrutiny they would face as standalone options.

The full report is available to subscribers on the MarketSage research portal. For more information about this report or any of ISS MI’s research offerings, please contact us.

By: Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence