While advisor interest in alternatives remains robust, advisors are becoming more selective about where they commit capital. The latest report in the ISS MI’s Advisor Pulse series focused on alternatives and captured increasing levels of adoption, with nearly half (48%) allocating to alternatives today and wirehouses continuing to lead. That headline, however, only goes so far, as changes in leading alternative strategies point to dynamic developments.

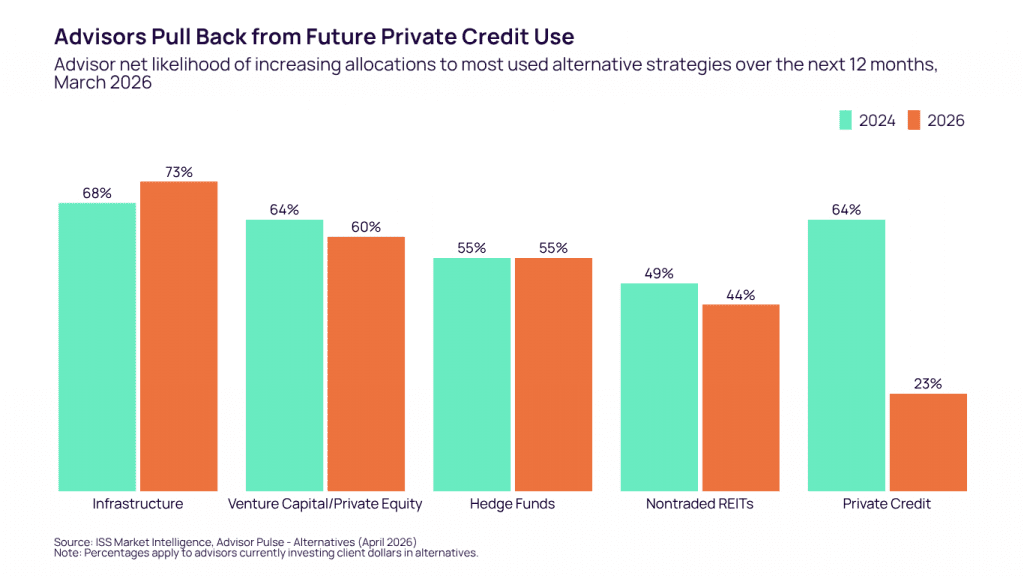

Private credit remains the most widely used strategy, with 60% of advisors invested, but the momentum behind it has slowed sharply. Just 23% now expect to increase allocations to the strategy over the next 12 months, down from 64% at the end of 2024. This shift was not reflected in other leading alternative strategies, as seen in the table above. Infrastructure, for example, saw 73% of advisors expecting to increase allocations over the next year, up from 68% in 2024.

Related: Growing Wave Toward Independence Gains Steam Amid Shifting Wealth Management Channels

Advisors have grown concerned about private credit following a series of negative headlines around bankruptcies and the heightened competition and vulnerability that private software firms face from artificial intelligence. This pullback stands to weigh on private credit managers and promote an increased focus by advisors on manager quality and downside protection. Even amid such pressure, advisors still on net demonstrated an intention to increase allocations to the strategy.

Developments in private credit have brought existing hurdles to alternatives adoption to the surface. Some investors seeking to withdraw from funds under pressure have come up against redemption gates. While these gates are often on semi-liquid funds, which themselves provide much greater liquidity than limited partnership structures, liquidity remains a paramount concern.

Related: The Advisor Trends Powering ETF Growth and Portfolio Outsourcing

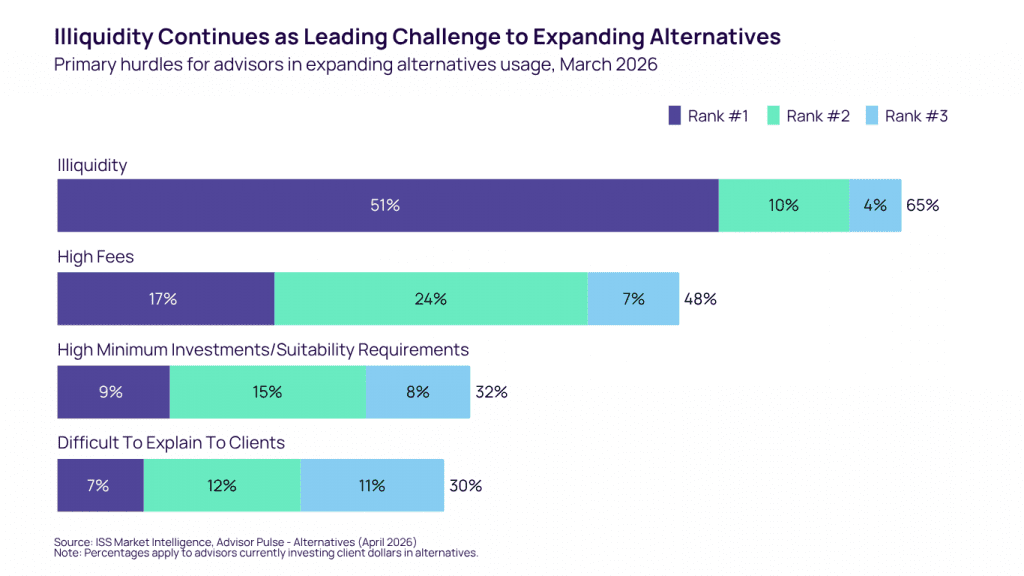

When asked about the primary hurdles to expanding the usage of alternatives, illiquidity stood out by a large margin. In fact, 65% of advisors cited it as one of their top three hurdles, with 51% saying it was the singular largest barrier to using more alternatives. Higher fees have served as a key driver for managers to offer more alternatives, though they stood out as the second highest hurdle for advisors at 47%.

Even as controversy has been heightened around the semi-liquid alternatives, surveyed advisors demonstrated the strongest interest in that structure. 39% of advisors stated that they most preferred to access alternatives through semi-liquid funds such as closed-end funds, interval funds, and business development companies, compared to 25% that chose limited partnership structures.

Related: 220 Active ETFs in One Quarter: The New Normal

The full Advisor Pulse report expands on these trends, exploring how adoption varies across advisor channels, what is driving increased usage, and how access, implementation, and client considerations are shaping real-world allocation decisions. See the full report, now available on the MarketSage research platform. For more information about this report, or any of ISS MI’s research offerings, please contact us.

Authors:

Alan Hess, Vice President, U.S. Fund Research, ISS Market Intelligence

Antara Maity, Senior Associate, U.S. Fund Research, ISS Market Intelligence